People usually ask this question when something has already gone wrong. A relapse abroad. A medical emergency that turns into a realisation. A family scrambling to understand what’s covered and what isn’t. The confusion is understandable, because insurance language is deliberately vague, and rehab sits in a grey zone that many policies quietly avoid spelling out.

Understanding the difference between travel insurance vs health insurance for rehab is not just about paperwork. It’s about knowing what kind of care is realistically accessible when addiction becomes a medical issue rather than a personal one.

What Rehab Is Considered to Be (Medically)

Rehabilitation for substance use is medical care. It involves detoxification, psychiatric assessment, therapy, monitoring, and often medication management. From a clinical standpoint, it falls under mental health and addiction treatment.

From an insurance standpoint, however, rehab is treated very differently depending on whether you’re dealing with health insurance for rehab or travel-related coverage.

That distinction is where most people get caught off guard.

How Health Insurance Covers Rehab Treatment

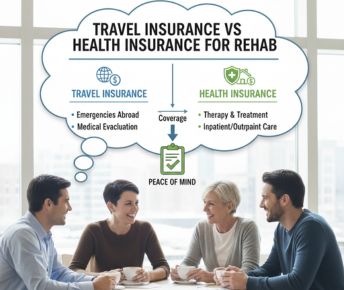

Most comprehensive health insurance policies recognise addiction as a medical condition. This is especially true for private health insurance rehab plans or employer-backed policies that include mental health coverage.

When rehab is covered, it is usually framed under:

- mental health treatment

- substance use disorder care

- inpatient or outpatient psychiatric services

This is why people ask does health insurance cover rehab or does health insurance cover alcohol rehab, because the answer depends on the policy’s mental health benefits, not on whether rehab is “special.”

Health insurance is designed to cover ongoing medical care. Rehab fits that category when it is deemed medically necessary.

What Health Insurance Usually Covers

Under appropriate policies, rehab health insurance may cover:

- medically supervised detox

- inpatient rehabilitation (partially or fully)

- outpatient programs

- psychiatric consultations

- therapy sessions

- medication management

Coverage often depends on:

- diagnosis

- duration limits

- network restrictions

- pre-authorisation

This is why drug rehab private health insurance plans tend to be clearer and more reliable than generic coverage.

Where Health Insurance Falls Short

Health insurance does not automatically mean “everything is paid for.”

Common limitations include:

- caps on inpatient days

- exclusion of luxury or non-medical services

- requirement that the rehab be medically accredited

- partial reimbursement rather than direct billing

Insurance will not cover rehab simply because someone wants it. It usually needs to be justified clinically.

That said, if someone is asking how to get insurance to pay for inpatient rehab, the answer is usually: documentation, diagnosis, and choosing a centre that understands insurance protocols.

What Travel Insurance Is Designed For

Travel insurance is built for short-term, unexpected events while traveling. Think accidents, acute illness, emergency hospitalisation, evacuation, or trip disruption.

It is not designed for long-term treatment planning.

This is the core misunderstanding behind travel vs health insurance in rehab contexts.

Travel insurance is reactive. Rehab is structured, ongoing care.

Does Travel Insurance Cover Rehabilitation Services?

In most cases, no.

Travel insurance may cover:

- emergency medical stabilisation

- short hospital stays

- emergency detox if life-threatening

- evacuation back to home country

What it does not usually cover is planned or extended rehabilitation.

This is why the question does travel insurance cover rehabilitation services almost always leads to disappointment. Rehab is classified as non-emergency, ongoing care, even if the addiction crisis feels urgent to the family.

WHY YOU SHOULD CHOOSE OUR REHAB

The Grey Area: Emergency vs Rehab

There is a narrow overlap.

If someone is hospitalised abroad due to overdose, withdrawal complications, or acute psychiatric crisis, travel insurance may cover the emergency hospital care. Once stabilised, however, continued rehab usually falls outside coverage.

At that point, insurers often push for repatriation rather than local rehab admission.

This is where families get stuck, assuming that emergency coverage extends into recovery. It rarely does.

Can You Use Health Insurance for Rehab While Traveling?

This depends on the policy.

Some international or global health insurance plans allow coverage abroad. Others require treatment within specific networks or countries.

If someone asks can I use my health insurance for rehab while traveling, the real question is whether the policy is:

- domestic-only

- international

- network-restricted

Many standard health insurance plans do not cover treatment outside the home country unless explicitly stated.

This is why people seeking insurance for rehab centers abroad often need separate international health coverage, not travel insurance.

Why Rehab Centres Ask About Insurance Early

Rehab centres that work with insurance are used to navigating these distinctions. They ask about:

- type of insurance

- country of coverage

- inpatient eligibility

- diagnosis history

This isn’t bureaucracy for its own sake. It determines whether admission is feasible or whether private payment is required.

Understanding insurance for rehab early prevents crisis-driven decisions later.

Private Payment vs Insurance: The Reality

Many people end up paying privately because:

- their insurance excludes addiction treatment

- travel insurance does not apply

- international coverage is unclear

This doesn’t mean insurance is useless. It means expectations need to be realistic.

Private rehab is not “better” by default. It is simply outside insurance systems.

The Bigger Mistake People Make

The biggest mistake is assuming insurance will “figure it out” during a crisis.

Insurance works best when:

- verified in advance

- pre-authorised

- aligned with the type of care needed

Waiting until relapse or emergency to check coverage almost always limits options.

What Actually Helps in Practice

If rehab may be needed:

- review health insurance mental health benefits

- confirm inpatient coverage specifically

- ask about international applicability if travel is involved

- speak directly to rehab admissions teams who understand insurance

Clarity upfront reduces chaos later.

FAQs

- How to get insurance to pay for inpatient rehab?

Choose a medically accredited centre, obtain a formal diagnosis, and ensure the insurer pre-authorises inpatient care under mental health or addiction benefits. - Does health insurance cover alcohol rehab?

Many policies do, under mental health or substance use treatment, but coverage varies by plan and limits. - Does health insurance cover rehab?

Often yes, but usually with conditions such as medical necessity, duration caps, and approved providers. - Does travel insurance cover rehabilitation services?

Generally no. Travel insurance focuses on emergency stabilisation, not long-term rehab. - Can I use my health insurance for rehab while traveling?

Only if the policy explicitly allows international treatment and includes rehab services.

How Can Samarpan Help?

At Samarpan Recovery Centre, we often guide families through the confusion around travel insurance vs health insurance for rehab, especially for international clients seeking treatment in Asia’s most trusted rehabilitation setting.

Many people assume standard travel insurance will cover addiction or mental health treatment, only to discover exclusions once a crisis arises. Health insurance, on the other hand, may offer partial coverage but often comes with limitations around psychiatric care, detox duration, or residential treatment.

This is where Samarpan’s experienced admissions and care coordination team steps in. We help clients clearly understand what their insurance does and does not cover, assist with documentation, and create transparent treatment plans so there are no financial surprises mid-recovery.

More importantly, Samarpan believes that access to care should never be delayed because of paperwork confusion. Whether a client is self-funded, insured, or travelling internationally for treatment, our focus remains the same: delivering world-class clinical care, safety, privacy, and continuity of treatment.

By combining clarity, ethical guidance, and flexible care pathways, Samarpan ensures that recovery is prioritised over policy fine print, allowing clients and families to focus on healing rather than logistics.